Information unaudited Information ungeprüftFinance and risk management

Framework

Assuming risk goes hand in hand with the business of banking. Sustainable and methodical finance and risk management is of crucial importance to ensure risk remains calculable. We, as the LLB Group, pursue a holistic approach. We attach great value to long-term financial management and forward-looking risk management at all levels of our organisation.

All risks that banks are exposed to are identified, assessed and monitored as part of risk management, whereby credit, market and operational risks in particular are taken into account. The aim is to maintain a balance between growth, opportunities and risks. In line with our holistic approach, risk management also includes the management of legal and compliance risks as well as information security.

The competences for the various areas of finance and risk management are bundled together in the Group CFO division.

Stability

Liechtenstein is one of the few countries in the world to have an AAA rating. In November 2024, the rating agency Standard & Poorʼs (S&P) reaffirmed the top rating for the countryʼs creditworthiness. According to the report, the renewed top rating reflects Liechtensteinʼs solid financial position and the high efficiency of its policies.

As a systemically important bank, we are subject to particularly strict financial market regulation and high capital requirements. With the implementation of the European Unionʼs Capital Requirements Directive (CRD V) and the establishment of the Deposit Guarantee and Investor Protection Foundation (EAS), Liechtenstein has a modern protection system that guarantees an adequate capital base and the protection of client deposits. For us as the LLB Group, too, a very solid capital base is a matter of course. We clearly exceed the required capital ratio (see paragraph Solid capitalisation).

Strategic expansion

As part of the ACT-26 corporate strategy, finance and risk management at the LLB Group has been significantly further developed in recent years. Particular attention has been paid to these topics:

- improvement in the efficiency of processes;

- prevention of money laundering, terrorist financing and sanctions circumvention;

- targeted strengthening of risk management.

The Group Business Risk Management department has been responsible for the management of operational risks since 2022. It comprises the areas of information security, data protection, cyber defence and the internal control system (see also the online special LLB in flux). In the 2024 financial year, we also created the new ‘Group Financial Crime Compliance’ division, which bundles measures to combat money laundering and the financing of terrorist and criminal activities as well as compliance with international sanctions. This emphasises the high priority of these processes within the LLB Group.

Financial management

The aim of our financial management is to create transparency at all levels of management in order that costs and income can be managed in line with corporate strategy in an efficient and timely manner. The key instruments used for this are:

- medium-term planning;

- the annual budgeting processes;

- key performance indicators from the Group’s management information system;

- the planning and management of capital and liquidity.

The tasks of financial management include the preparation of the annual financial statements as well as meeting regulatory reporting requirements (see also chapter Accounting principles).

Risk management

We, as the LLB Group, have a prudent approach to risk. This is of paramount importance for our reputation, our excellent financial strength and our sustainable profitability. Based on our risk policy, our risk management encompasses the following aspects:

- systematic identification and assessment;

- reporting;

- management and monitoring of all material risks;

- asset liability management (ALM).

We have an appropriate organisational and methodological framework for assessing and managing risk (see chapter Risk management in the financial section).

Responsibility for the management of operational risks lies with the Business Group Risk Management Department. It covers the areas of:

- information security;

- data protection;

- cyber defence;

- the internal control system.

Liquidity management

The LLB Group has in place robust strategies, policies, processes and systems that enable it to identify, measure, manage and monitor liquidity risk. The internal liquidity adequacy assessment process (ILAAP) is set down in internal regulations and guidelines and is reviewed annually (see chapter Risk management in the financial section). The Group Treasury manages risks in the banking book that result from banking activities.

Capital management

Within the LLB Group, we have in place robust, comprehensive and effective processes to assess and ensure adequate equity capital on an ongoing basis. The internal capital adequacy assessment process (ICAAP) is a key risk management instrument here. The ICAAP is documented in internal regulations and guidelines and is reviewed and revised annually on the basis of overall bank stress tests.

Solid equity base

Having an equity base that is of a sufficiently high quality is integral to our identity as the LLB Group. For a solid equity capital base not only protects its reputation, but is also part of the economic and financial credibility of a bank. Furthermore, our financial strength shall remain, as far as possible, unaffected by fluctuations in the capital markets.

Since LLB is considered systemically important in Liechtenstein, we are subject to a regulatory minimum capital adequacy ratio of 13.7 per cent. As part of our strategy, we are targeting a Tier 1 ratio of over 16 per cent.

Financial strength is confirmed

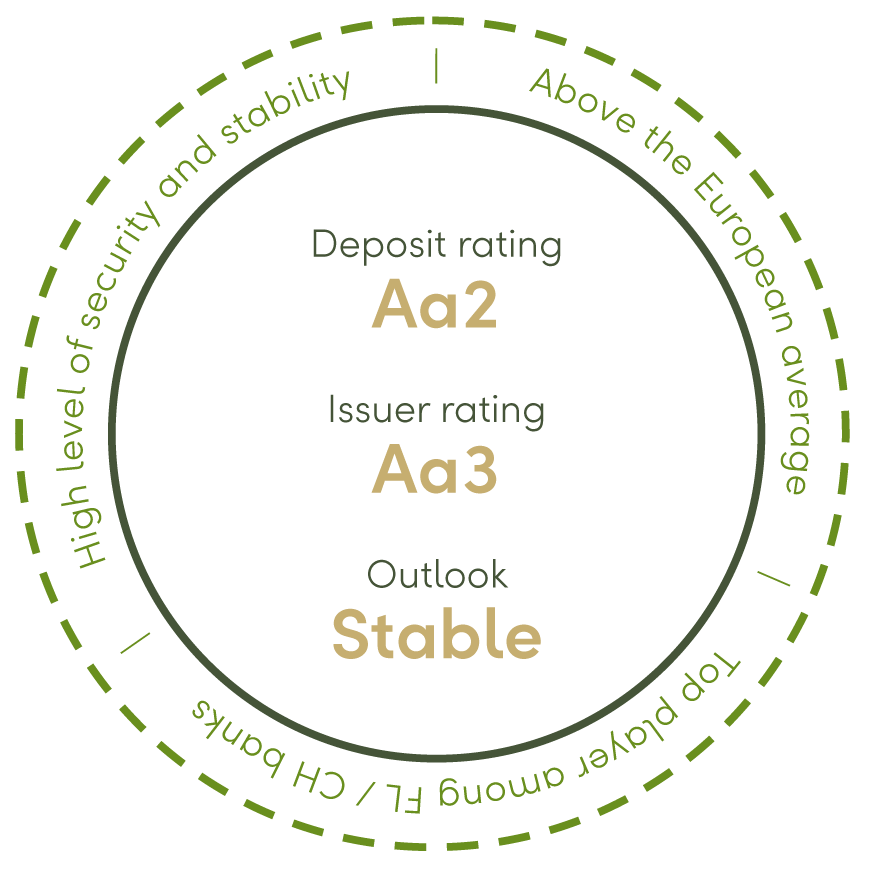

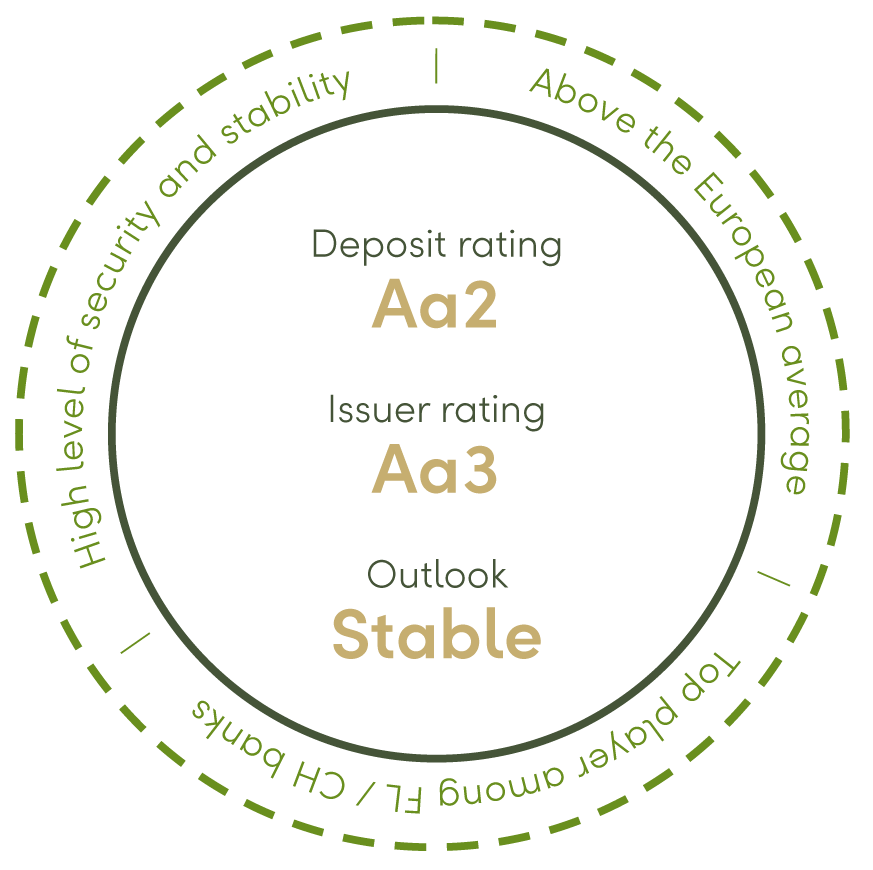

Liechtensteinische Landesbank has a deposit rating of Aa2 from rating agency Moody’s. Following the announcement of the acquisition of ZKB Österreich (see Letter to shareholders), the rating was reviewed and reconfirmed in July 2024. This makes us, according to Moody’s, one of the highest-rated banks in the world and places us in the top league of Liechtenstein and Swiss banks, ranking us well above the average for European financial institutions.

Moody’s rating also underlines LLB’s stability and financial strength. It is proof of our prudent finance and risk management.

Credit management

As Liechtensteinische Landesbank, helping private individuals, companies and public institutions to finance and realise their plans for the future is integral to our identity.

Independent credit decisions

At the LLB Group, authorisation to grant loans is based on level of knowledge and experience and type of loan. With the exception of standard business transactions, the authority to grant credit lines lies with the back office, i.e. Group Credit Management and the superordinate Credit Committees. Credit decisions are thus made independently of market pressures and market targets. In this way, we are able to avoid conflicts of interest and ensure that risks in each and every case are assessed in an objective and independent manner.

High standards of lending

We, as the LLB Group, pursue a risk-conscious credit policy. In doing so, we rely on:

- the differentiated and separate assessment of loan applications;

- the risk-oriented assessment of collateral values;

- the individual assessment of affordability;

- the consideration of standard equity requirements.

These different control processes help us to act in a risk-conscious manner.

Compliance risks

The LLB Group’s compliance organisation is part of risk management and focuses on dealing with legal risks and three other areas:

- Combating money laundering and financing of terrorism as well as complying with international sanctions;

- Implementing tax compliance within the framework of international agreements and complying with local tax legislation;

- Complying with supervisory requirements, specifically dealing with conflicts of interest and monitoring employee transactions.

There are three lines of defence against risks:

- First line: The first line of defence covers all functions that are involved in conducting day-to-day business operations and, as a rule, assigned with a results-based objective.

- Second line: The second line of defence – this includes the LLB Groupʼs compliance organisation – carries out, independently of the market and the results, monitoring and control functions, and is responsible for ensuring compliance with applicable internal and external requirements.

- Third line: In the third line of defence, the internal audit ensures the effectiveness of the controls.

Combating money laundering and financing of terrorism as well as complying with international sanctions

Combating money laundering and terrorist financing along with complying with international sanctions are given the highest priority in the LLB Group. To underscore their importance and further minimise the risk of the LLB Group being misused for criminal purposes, we created a separate business area – Group Financial Crime Compliance – for the efficient and effective handling of these issues with effect from 1 January 2024.

The LLB Group has in place robust programmes to prevent financial crime. These include regulations, system-supported processes and the use of IT tools and apply both when establishing new or monitoring existing business relationships. Transaction monitoring is systematic and risk-oriented.

In order to ensure compliance with international sanctions and to prevent circumvention of sanctions, the LLB Group has implemented a comprehensive sanctions compliance programme under which we continuously monitor geopolitical developments and take prompt action in the event of any changes.

We provide regular training within the LLB Group to ensure that employees stay informed about the latest regulatory changes.

Managing conflicts of interest

Handling conflicts of interest professionally is an essential part of trustworthy, values-based corporate management. During the reporting year, we tightened the relevant rules for our corporate bodies and employees, with the intention being to protect our bank’s stakeholders from potential conflicts of interest. Should conflicts of interest nevertheless arise, the new set of rules provide a basis for managing them as well as possible. We expect our executive bodies and employees to comply with applicable laws, regulations and guidelines, professional standards and our ‘Rules of Conduct’. These rules contain information on which transactions with financial instruments are not permitted for employees and executive bodies. In addition, general principles for employee transactions are defined, as is the handling of conflicts of interest. The handling of business relationships between employees and executive bodies is clearly regulated, as are the acceptance of benefits and the exercise of secondary employment.

Dealing with cyber risks

Protection against cyber attacks remains of crucial importance to us. It is based on modern IT systems as well as properly trained and aware employees. The information security requirements are set out in guidelines that apply throughout the company and are consistently implemented through technical and organisational measures. Any new regulatory requirements, such the Digital Operational Resilience Act (DORA), as well as best practice standards are taken into account when developing and implementing these measures. Our data is fully protected by effective processes and advanced technologies. Experts continuously monitor for cyber threats and take risk-based defensive measures. These measures are constantly being expanded by the LLB Group’s Cyber Defence Center. Structured vulnerability management and periodic attack simulations ensure a permanently high level of security (see also the online special LLB in flux).

Internal control system

The internal control system (ICS) is as an integral part of our Group-wide risk management. It contributes to increasing risk transparency in the company by monitoring the risks in the relevant business processes through effective control processes. These controls are guided by industry standards.

Business continuity management (BCM)

In a crisis or catastrophe, decisions have to be made that cannot be dealt with using the resources ordinarily available to management. Business continuity management (BCM) comes into play whenever preventative measures defined in the risk management process do not work and the level of damage from an event could assume a scale that threatens the existence of the company. It identifies business-critical processes within the whole LLB Group, establishes BCM crisis teams, draws up emergency plans and keeps senior management up to date with regular reports. Events in recent years, such as the power shortage and the corona pandemic, have shown the LLB Group’s BCM to be crisis-proof, efficient and comprehensive.