Finance and risk management

Information unaudited Information ungeprüft Finance and risk management

All risks a bank is exposed to are identified, assessed and monitored as part of risk and finance management, whereby credit, market and operational risks in particular are taken into account. The aim is to minimise these risks as far as possible and at the same time to ensure the financial stability of the bank.

We attach great importance to sustainable financial and forward-looking risk management at all levels of our organisation. In doing so, we pursue a holistic approach that has proven its worth. Risk management therefore also includes the management of legal and compliance risks as well as information security. The competences for the various areas of finance and risk management are bundled together in the Group CFO division. The central task of the division is that of maintaining a balance between growth, opportunities and risks.

Strategic expansion

As part of the ACT-26 corporate strategy, finance and risk management is being developed further with the main focus being on the:

- improvement in the efficiency of processes;

- targeted strengthening of risk management;

- scaling up of cyber defence;

- expansion of data protection.

Responsibility for the management of operational risks has lain since 2022 with the Business Risk Management Department. It covers the areas of information security, data protection and cyber defence as well as the internal control system. The 2024 business year also sees the creation of our new business area, “Group Financial Crime Compliance”, which bundles together measures to combat money laundering and the financing of terrorism and criminal activities as well as to comply with international sanctions. Its creation reflects the high priority we assign to these processes in the LLB Group.

“The banking business is naturally associated with risks. That is why we attach great importance to forward-looking financial and risk management at all levels of our organisation.”

Financial management

The aim of our financial management is to create transparency at all levels of management in order that costs and income can be managed in line with corporate strategy in an efficient and timely manner. The key instruments are medium-term planning, the annual budgeting process, the key performance indicators from the Group’s management information system, and the planning and management of capital and liquidity.

The tasks of financial management also include preparing the annual financial statements in accordance with local law and the International Financial Reporting Standards (EU-IFRS) applicable in the European Union (EU) as well as ensuring regulatory reporting.

Risk management

We, as the LLB Group, have a prudent approach to risk. This is of paramount importance when it comes to protecting our reputation, maintaining our excellent financial strength and safeguarding our sustainable profitability. Based on our risk policy, our risk management encompasses the systematic identification and assessment, reporting, management and monitoring of credit, market, liquidity and operational risks, as well as asset liability management (ALM). The LLB Group uses an appropriate organisational and methodological framework for assessing and managing risk (see chapter Risk management in the financial section).

Combating money laundering and the financing of terrorist or criminal activities as well as complying with international sanctions are given the highest priority in the LLB Group. Creating a dedicated business area in 2024 in which to bundle these activities together demonstrates our commitment to minimise regulatory risks.

Liquidity management

The LLB Group has in place robust strategies, policies, processes and systems that enable it to identify, measure, manage and monitor liquidity risk. The internal liquidity adequacy assessment process (ILAAP) is set down in internal regulations and guidelines and is reviewed annually (see chapter Risk management in the financial section). Key liquidity figures are published in the chapter Regulatory disclosures. The Group Treasury manages risks in the banking book that result from banking activities, especially liquidity, interest rate and foreign currency risks.

Capital management

The LLB Group has in place sound, comprehensive and effective processes to assess and maintain adequate equity capital on an ongoing basis. The internal capital adequacy assessment process (ICAAP) is a key risk management instrument. The ICAAP is documented in internal regulations and guidelines and is reviewed and revised annually on the basis of overall bank stress tests.

Solid equity base

A good equity capital base not only protects its reputation, but is also part of the economic and financial credibility of a bank. Having an equity base that is of a sufficiently high quality is therefore integral to our identity. Our financial strength shall remain, as far as possible, unaffected by fluctuations in the capital markets.

Since LLB is considered systemically important in Liechtenstein, we are subject to a regulatory minimum capital adequacy ratio of 13.7 per cent. We are targeting a tier 1 ratio of over 16 per cent as a strategic objective. We report our capital ratio in the chapter Regulatory disclosures.

Thanks to our solid equity base, which consists entirely of hard core capital, we, as the LLB Group, continue to enjoy a high level of financial stability and security. This comfortable capital situation gives us scope for further acquisitions.

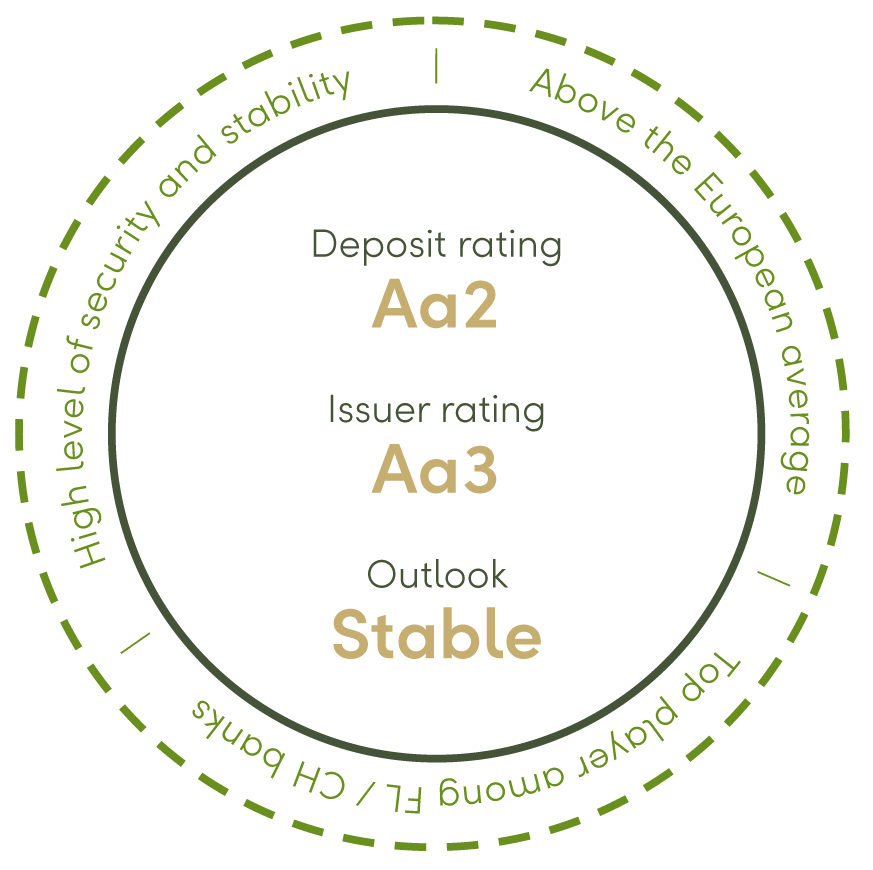

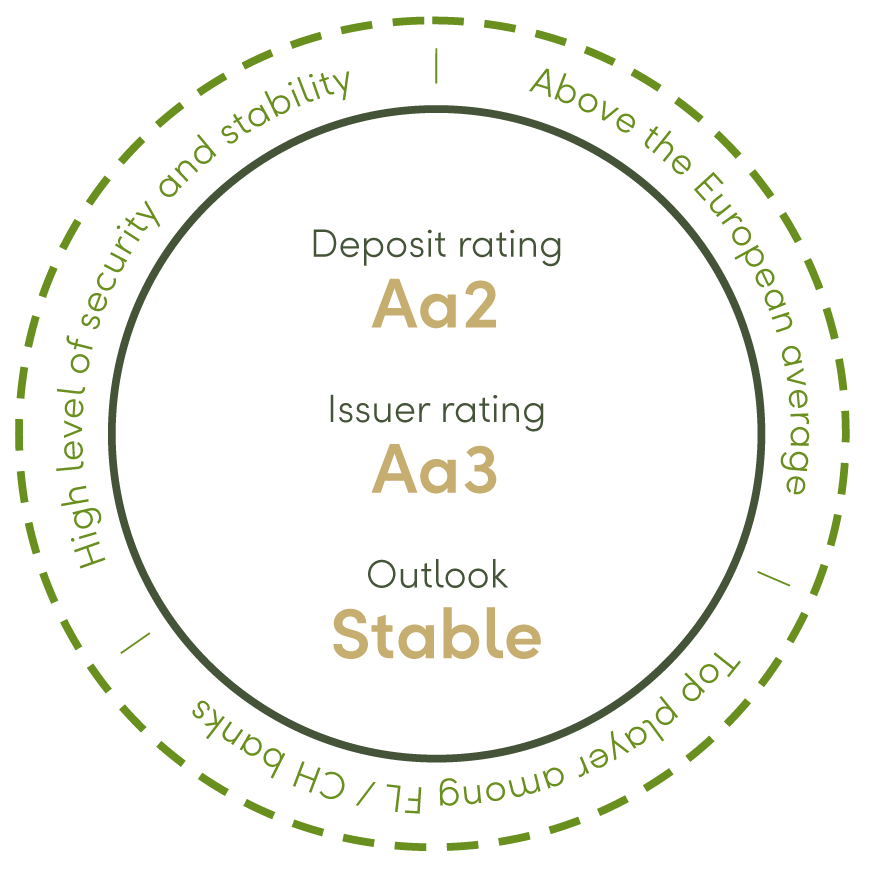

Rating confirms financial strength

Liechtensteinische Landesbank has a deposits rating of Aa2 from rating agency Moody’s. The rating was reaffirmed in autumn of the reporting year. This makes us, according to Moody’s, one of the highest-rated banks in the world and places us in the top league of Liechtenstein and Swiss banks and ranks us well above the average for European financial institutions. The rating underlines LLB’s stability and financial strength. It is proof of our prudent finance and risk management.

Credit management

We help private individuals, companies and public institutions to finance and realise their plans for the future.

At CHF 13.8 billion, the lion’s share of loans made during the reporting year, namely 90.3 per cent (31.12.2022: 89.2 %), comprised loans secured by mortgages. We continued to successfully grow our market share of loans to clients. At the end of 2023, the volume of loans had increased to CHF 15.3 billion (31.12.2022: CHF 14.4 billion). We extend mortgages primarily in the market regions of Liechtenstein, north-eastern Switzerland and the region of Zurich.

Independent credit decisions

At the LLB Group, authorisation to grant loans is based on level of knowledge and experience and type of loan. With the exception of standard business transactions, the authority to grant credit lines lies with the back office, i.e. Group Credit Management and the superordinate Credit Committees. Credit decisions are thus made independently of market pressures and market targets. In this way, we are able to avoid conflicts of interest and ensure that risks in each and every case are assessed in an objective and independent manner.

High standards with lending

We, as the LLB Group, pursue a risk-conscious credit policy. To this belongs the differentiated and separate evaluation of loan applications, the conservative assessment of collateral values, the individual assessment of affordability as well as consideration of standard equity requirements. The various control processes help us to reliably fulfil our performance mandate and to act in a risk-oriented manner (see chapter Our understanding of sustainability).

Compliance risks

The LLB Group’s compliance organisation focuses on dealing with legal risks and three other areas:

- Combating money laundering and financing of terrorism as well as complying with international sanctions;

- Implementing tax compliance within the framework of international agreements and complying with local tax legislation;

- Complying with regulatory requirements, monitoring employee transactions and dealing with conflicts of interest.

The compliance organisation is part of risk management at the LLB Group. There are three lines of defence against risks:

- The first line of defence covers all functions that are involved in conducting day-to-day business operations and, as a rule, have results-based objectives.

- The second line of defence – this includes the LLB Group’s compliance organisation – carries out, independently of the market and the results, monitoring and control functions, and is responsible for ensuring compliance with applicable internal and external regulations.

- In the third line of defence, the internal audit ensures the effectiveness of the controls.

Combating money laundering and terrorist financing

We address the risks of money laundering and terrorist financing with a strict, IT-supported process. This applies both when establishing new or monitoring existing business relationships. Transactions are controlled systematically and according to risk. The importance of these processes is underlined by our creation of a new business area in 2024.

We restrict our active market development to our home markets of Liechtenstein, Switzerland and Austria and for our cross-border business to regions that are strategically and economically significant to LLB. This means the markets of Germany and the rest of Western Europe, the growth markets of Central and Eastern Europe, as well as the Middle East.

Through internal regulations and training, we ensure that within the LLB Group employees are regularly informed about regulatory changes, sensitised to indications of possible money laundering, and know and comply with the regulations of the respective target country when engaging in cross-border activities.

Rules of conduct

We expect our corporate bodies and employees to comply with applicable laws, regulations and guidelines, professional standards and our rules of conduct. These contain information on which transactions in financial instruments are not permitted for employees and corporate bodies. They also set out the general principles for employee transactions and for dealing with conflicts of interest. The acceptance of inducements and the exercise of secondary employment are also clearly regulated.

Dealing with cyber risks

Protection against attacks from the internet continues to be a high priority for us. It is ensured through IT systems and trained and aware employees. The information security requirements are set out in guidelines that apply throughout the company and implemented through technical and organisational measures. Our data is protected by robust processes and advanced systems. Specialists continuously analyse new cyber threats and, depending on the risk, take appropriate defensive measures. These measures are constantly being expanded by the LLB Group’s Cyber Defence Center. Through targeted vulnerability management and penetration tests we ensure a consistently high level of security.

Internal control system

The internal control system (ICS) is as an integral part of our Group-wide risk management. It contributes to increasing risk transparency in the company by monitoring the risks in the relevant business processes through effective control processes. These controls are guided by industry standards.

Business continuity management (BCM)

In a crisis or catastrophe, decisions have to be made that cannot be dealt with using the resources ordinarily available to management. Business continuity management (BCM) comes into play whenever preventative measures defined in the risk management process do not work and the level of damage from an event could assume a scale that threatens the existence of the company. It identifies business-critical processes within the whole LLB Group, establishes BCM crisis teams, draws up emergency plans and keeps senior management up to date with regular reports. This was the case in the recent past in connection with the electricity shortage and before that with the corona pandemic. The LLB Group’s BCM has been shown in these instances to be crisis-proof, efficient and comprehensive.